Susan Hyttinen | Mikko Mäntylä

Going public – a series by accel & soaked by slush – article IV

In our content series with Accel, we’ve talked a lot about going public, and the different routes to take. Here’s what European founders and operators themselves had to say.

#1: Should I Stay or Should I Go? European startup founders want to exit through taking their companies public, but this desire increases in later stages of growth

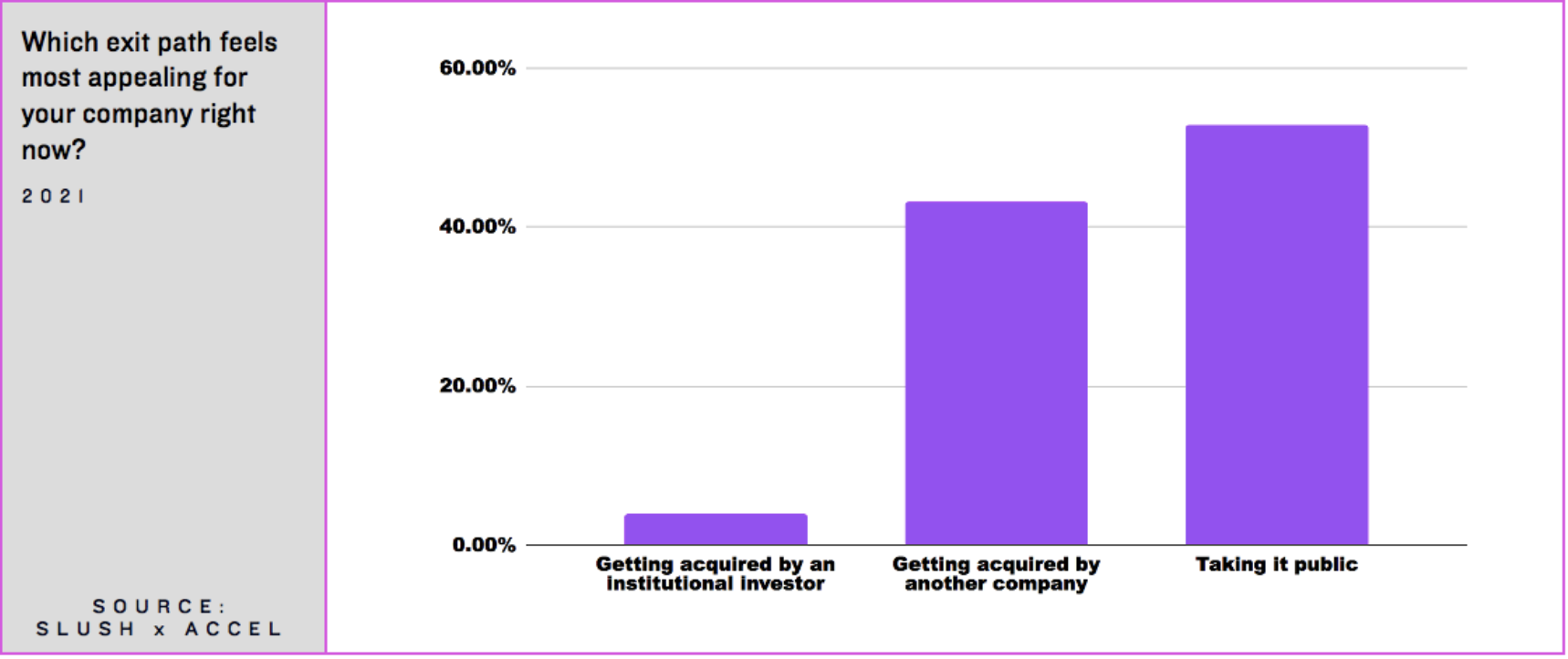

Which exit path to take? For the European startup founders in our dataset, taking companies public is more popular than being acquired, with a slight overall majority of 52.9%. Getting acquired by another company is a strong second with 43.3%, whereas acquisition by an institutional investor isn’t a popular alternative, with only 3.9% of founders preferring this option.

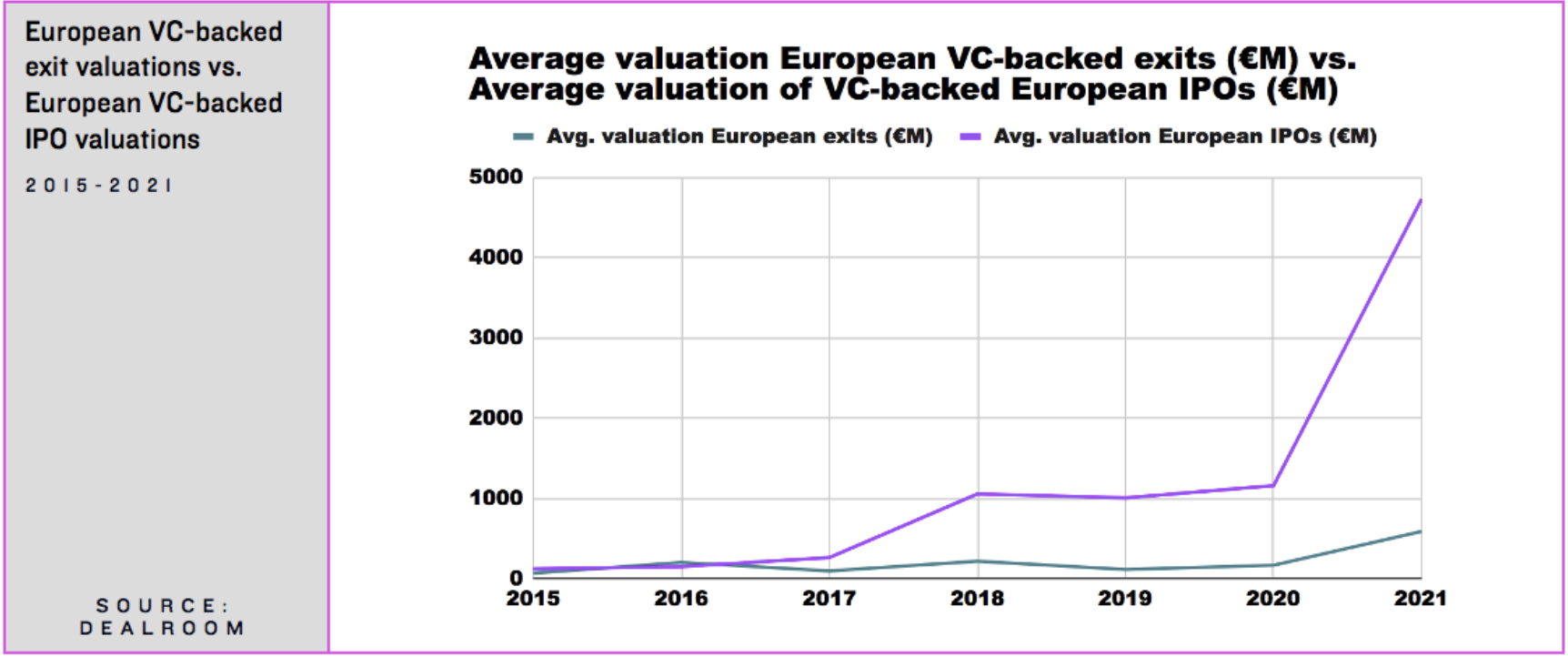

To some extent taking companies public may be more popular due to them being more financially lucrative. This is evident when looking at Dealroom data on the valuations of European VC-backed exits in general, and then comparing them with the sub-cohort of IPOs during 2015-2021*: average valuations of exits in this period were on average €173.6M, the corresponding figure being 699.2M for IPOs. As visible in the graph below, the difference in valuation between European exits and IPOs has become increasingly pronounced from 2017 onwards, and exploded in the first months of 2021 with major IPOs like those of UiPath and Deliveroo.

European founders’ keenness to go public is stronger than the actual proportion of companies that exit through this method; Dealroom data shows that whereas there were 2,545 exits of VC-backed companies in Europe in 2015-2021, only 10.0% (251) of these were through IPOs (the dataset excluding SPACs, of which there has been a negligent amount to date in Europe). The desire to go public is definitely there, even if reality hasn’t quite caught up with European founders’ dreams.

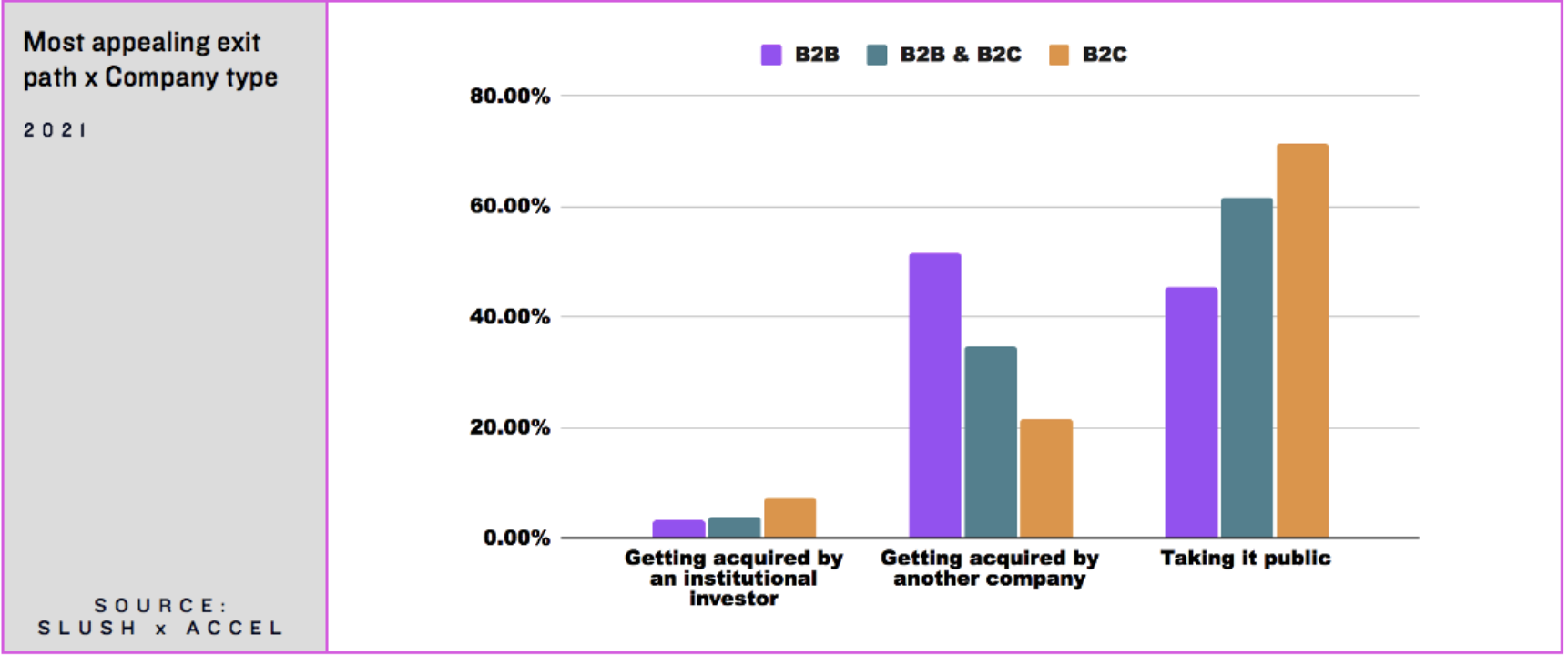

When comparing this data with company type (B2B, B2C, or mixed), it is evident that B2B companies are much more likely to find acquisition an appealing route with a 51.6% preference, whereas B2C companies are by far most likely to want to take their companies public (71.4%).

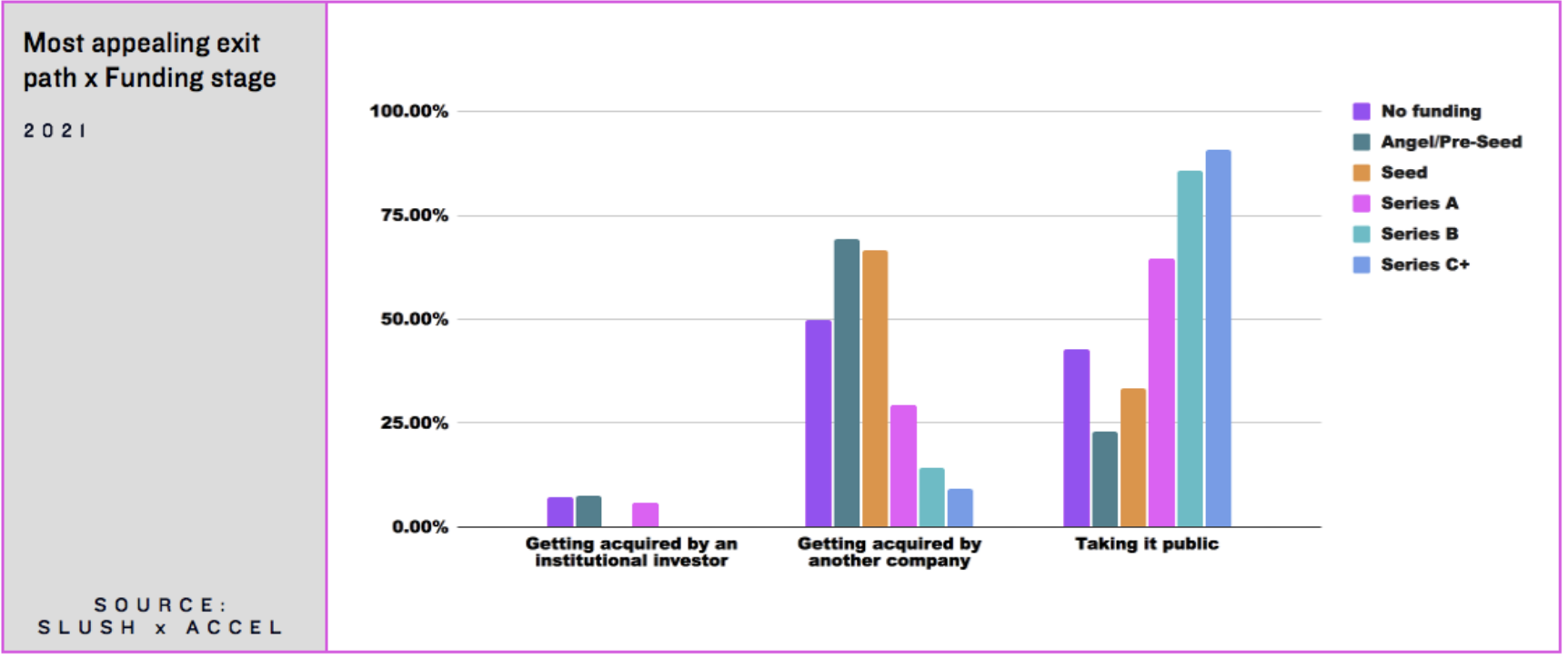

The more light there is at the end of the tunnel, the more startups want to exit by going public. When looking at different funding rounds, general intuition seems to hold – the later the stage of the company, the more likely it is that a founder wants to go public, with the inclination being the greatest in Series C+, with 90.9% of respondents in this group preferring this option.

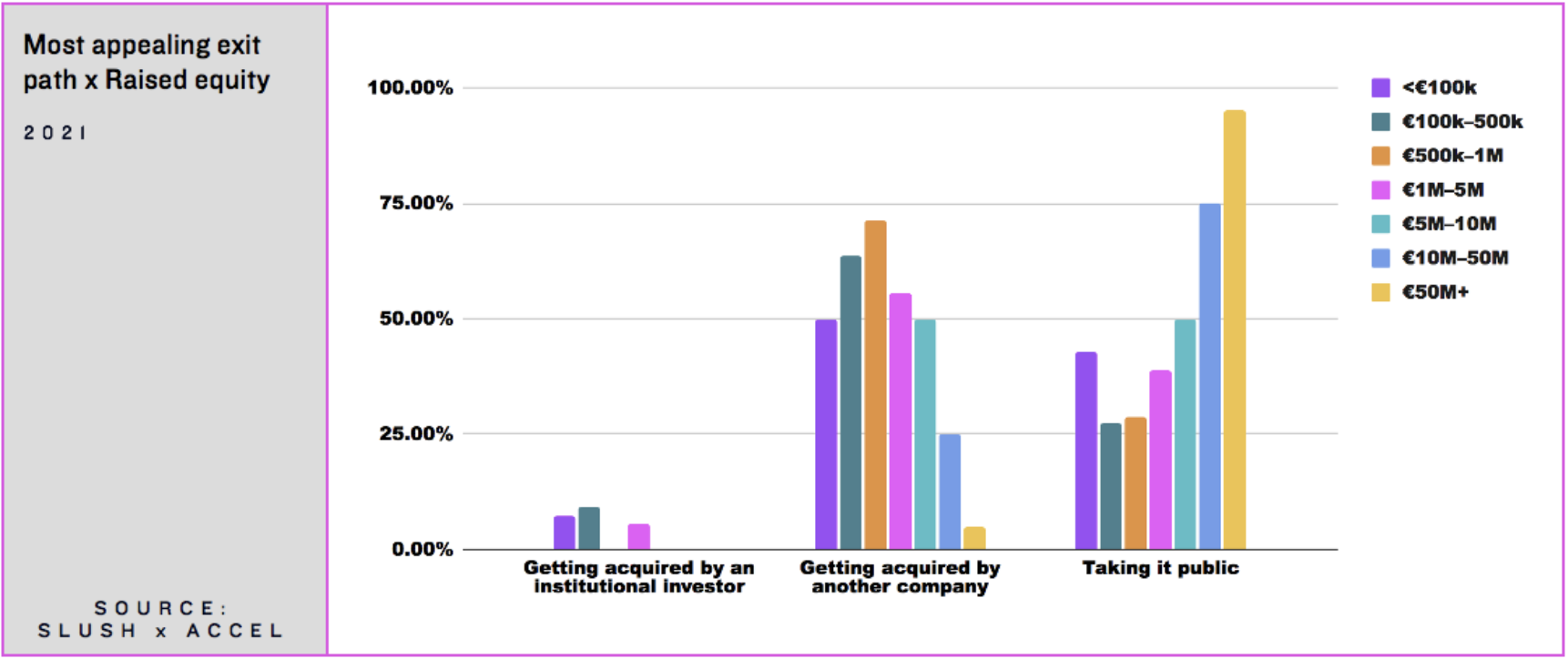

A similar trend is visible concerning the amount of equity raised; after the €500k-1M mark, the desire to be acquired decreases, and startup founders want to take their businesses public.

#2: How? The traditional IPO route still reigns large – but SPACs are catching up

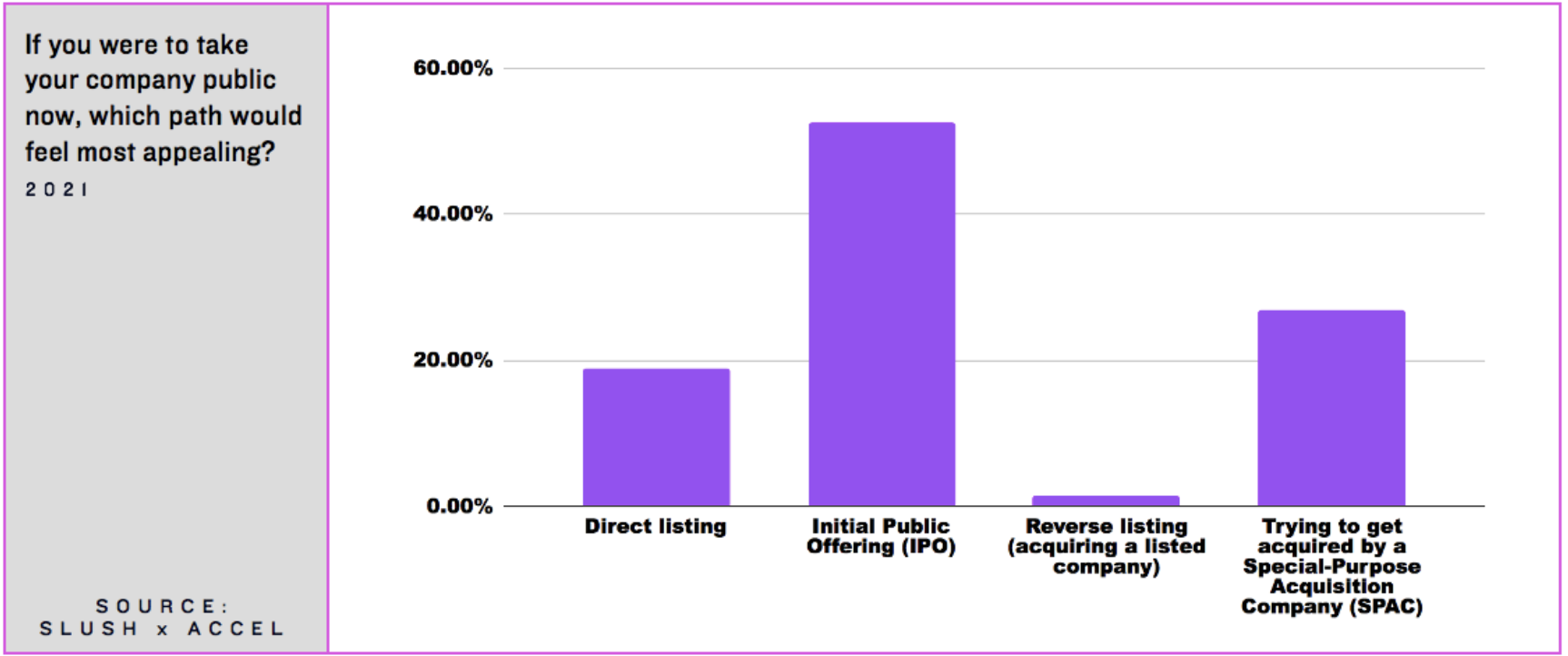

There are now more options than ever for going public, with very case-specific pros and cons. In our survey, the traditional option of going public through an IPO remains the most popular option, with over half of startups (52.6%) preferring this option.

SPACs have their origins in the ‘blank-check companies’ of the 1980s, fully kicking off in the US in the past year with 230 SPAC IPOs completed, and a whopping $71 billion raised – the most ever. While the SPAC trend hasn’t quite caught up with Europe as of yet, the hype sure has. The emergent SPAC craze is visible in it having taken over the option of direct listing (innovated by Spotify in 2018) in our survey, accruing 27.0% and 19.0%, respectively. With 1.5%, the appetite for reverse listing (also known as backdoor listing or reverse acquisition) is by far the lowest.

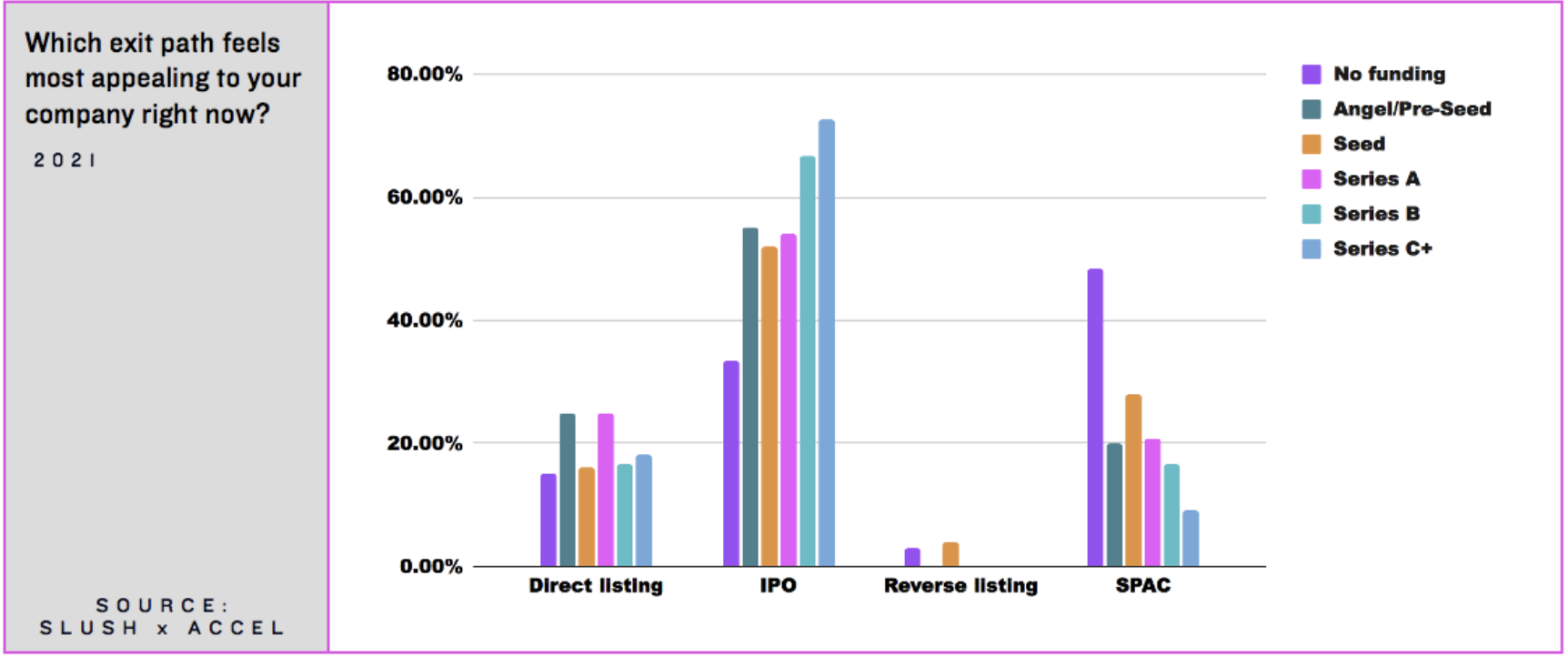

Relative to stages of growth, the appetite for SPACs seems to be higher in the earlier stages. Inversely, the popularity of IPOs increases as startups mature.

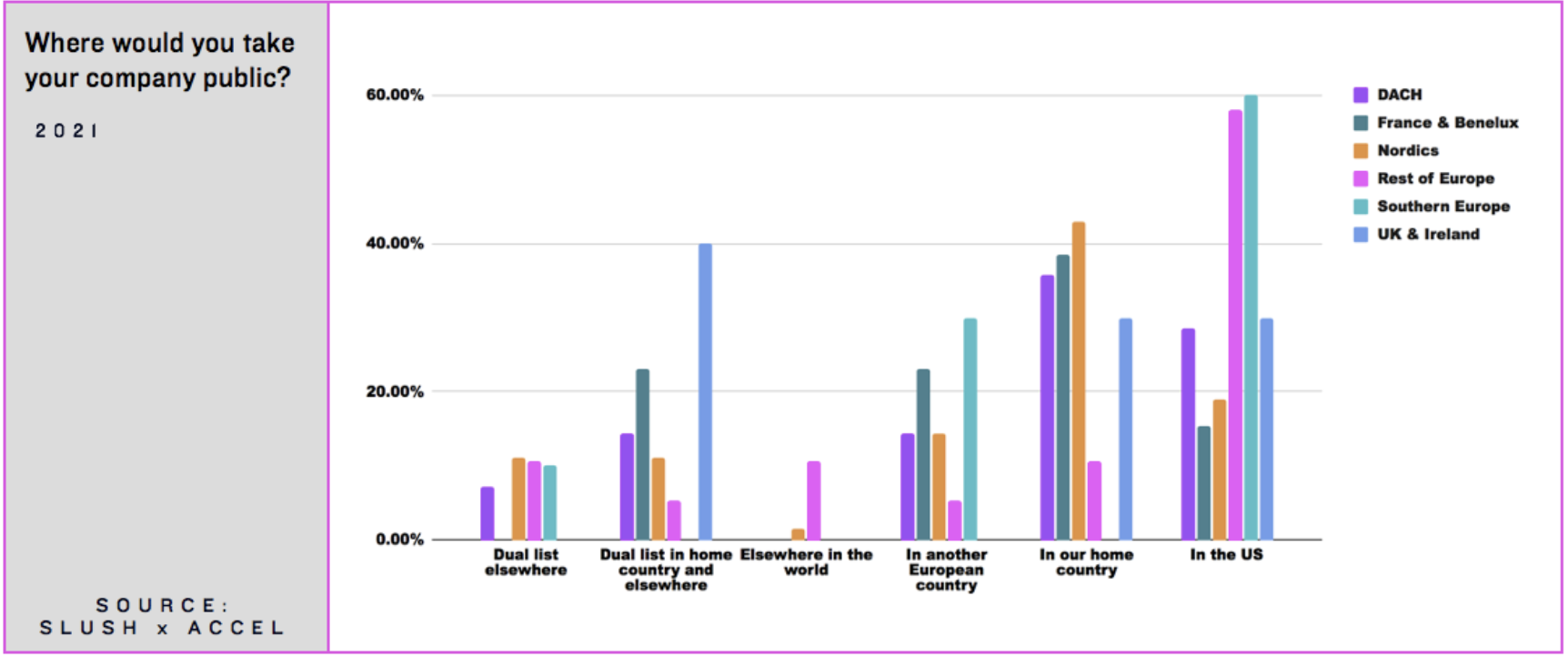

#3: Where? Nordic countries like to list at home – for good reasons

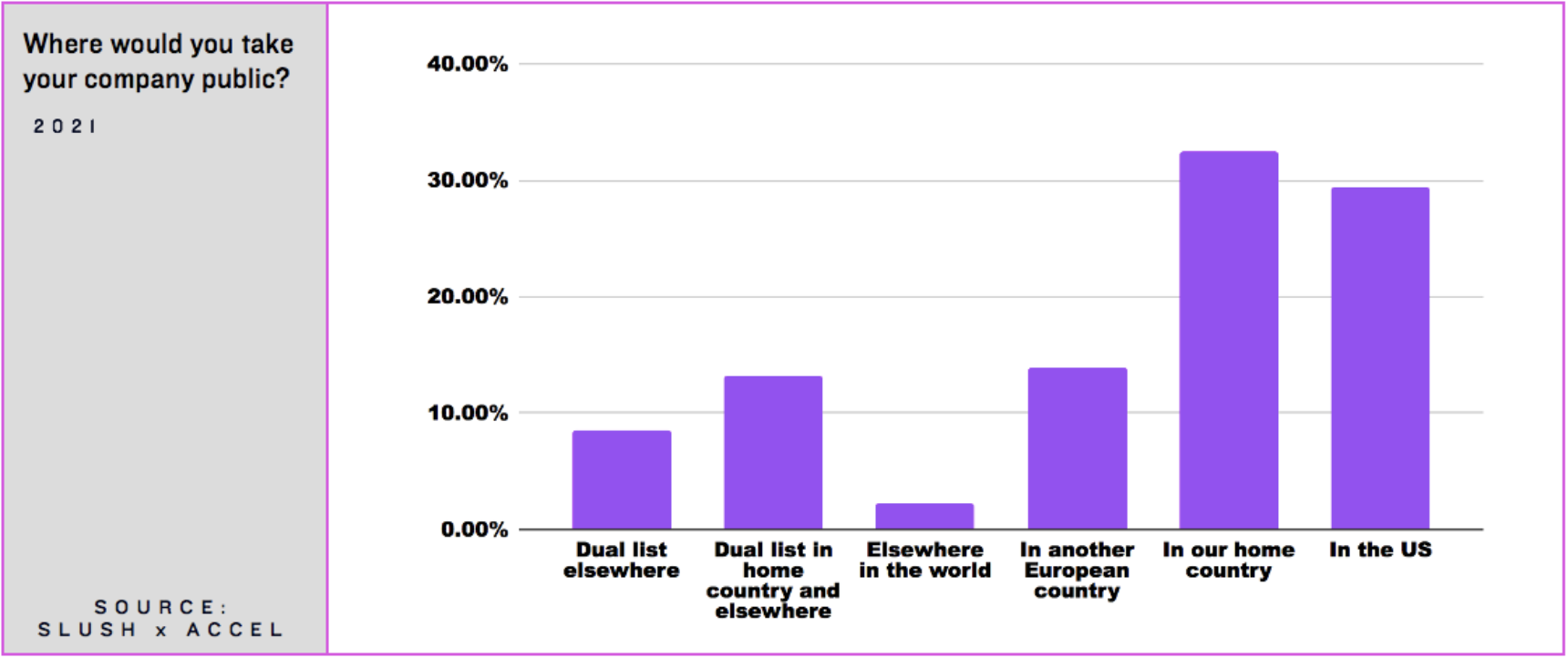

Location, location, location… The European startup founders in our survey clearly have a taste for their home countries and the US, with 32.6% being for listing in their home country, and 29.5% preference for the US. When it comes to countries outside of the US and Europe, interest seems to be faltering.

Dual listing altogether accounts for 21.7% of founders’ location preferences, the viability of this option probably being an implication of the attractiveness of the US as the most likely location for a dual listing due to the size of its economy and capital markets.

Some variation exists between different regions in terms of where they want to list. For instance, UK and Ireland only want to list in their home countries, in the US, or dual list…most likely in their home country and the US due to the latter’s attractive markets. In our dataset, home country listing is most popular for Nordic countries, which also happened to rule the European IPO game in 2020, aided by transparent markets, technology focus, and early commitments by investors in the region.

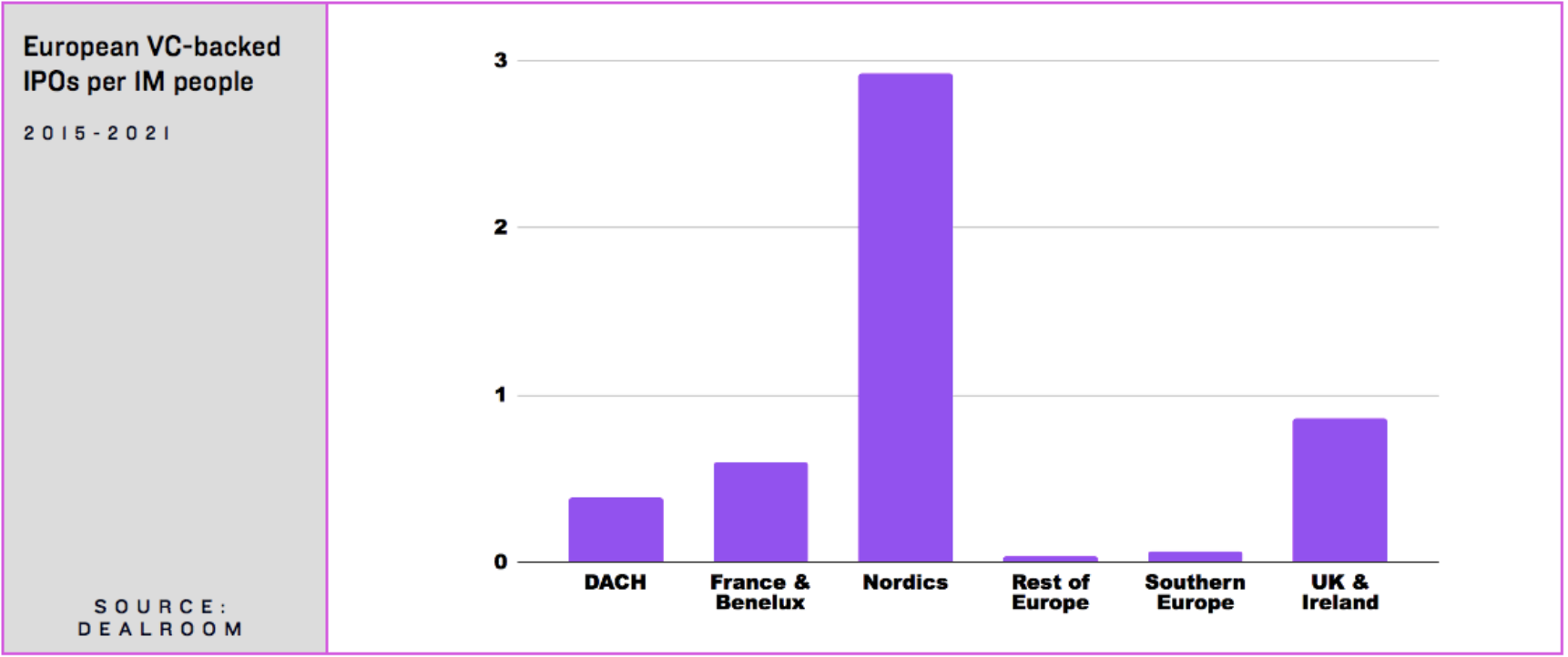

According to Dealroom data, Nordic countries had the most IPOs in Europe in 2015-2021* (80), followed by the UK & Ireland (61), France & Benelux (58), DACH (39), Southern Europe (10), and Rest of Europe (9). When further comparing different regions on their VC-backed IPOs per capita, Nordic countries are clearly set apart with 2.9 VC-backed IPOs to 1M people. In comparison, the second-highest number is that of the UK & Ireland with 0.86 VC-backed IPOs per 1M people.

#4: When? Your company doesn’t need to be a unicorn to go public (and European founders know this)

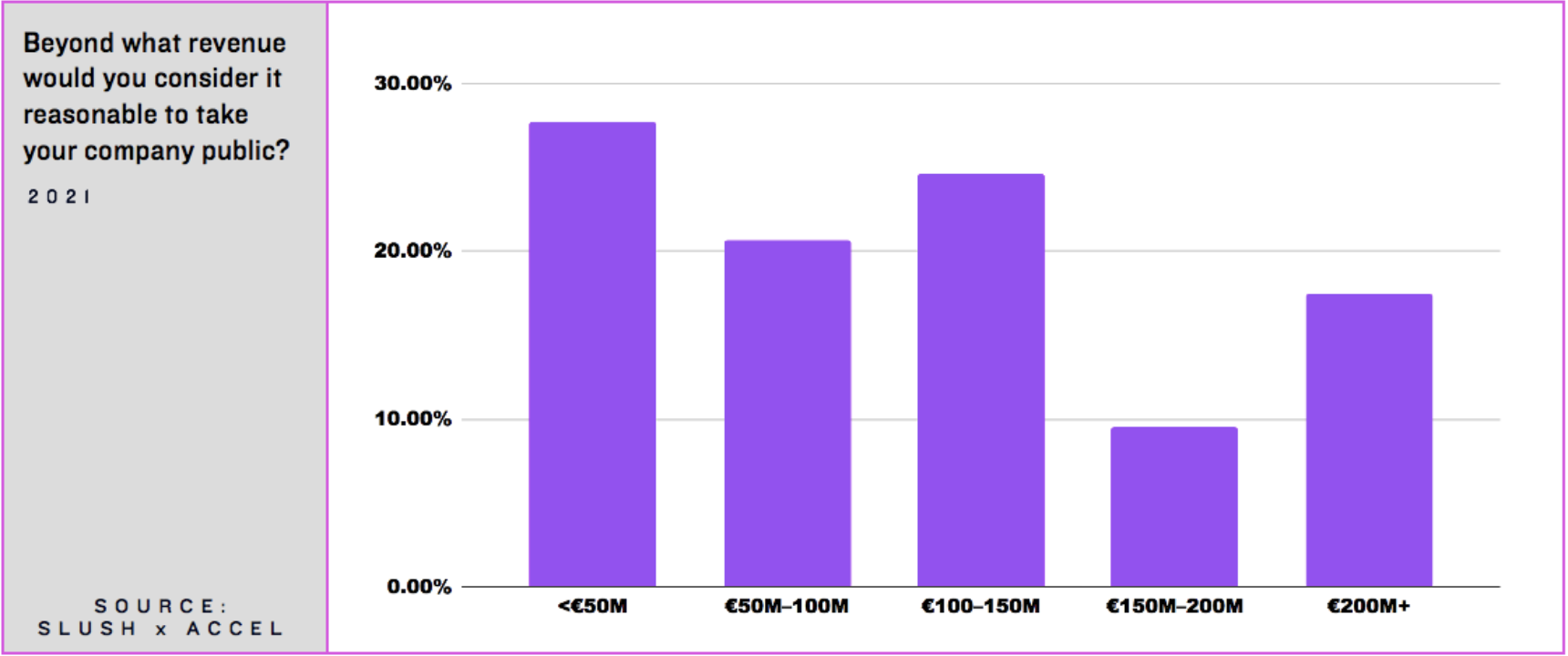

Deciding when to go public can be a daunting decision to make; there are various things to consider, ranging from whether your finance function is up to par to your board being ‘public ready’. Our survey examined European founders’ judgment on how reasonable they thought going public was through the quantitative metrics of valuation and revenue.

Looking at revenue, the data is distributed somewhat evenly across the different categories. This could be explained by the fact that no ‘golden rule’ for where your revenue should be when going public exists. While there has been much talk of the 100M revenue threshold in the past, other considerations such as growth prospects, competitive landscape, and the predictability of revenue flow and the business itself, weigh in on the equation.

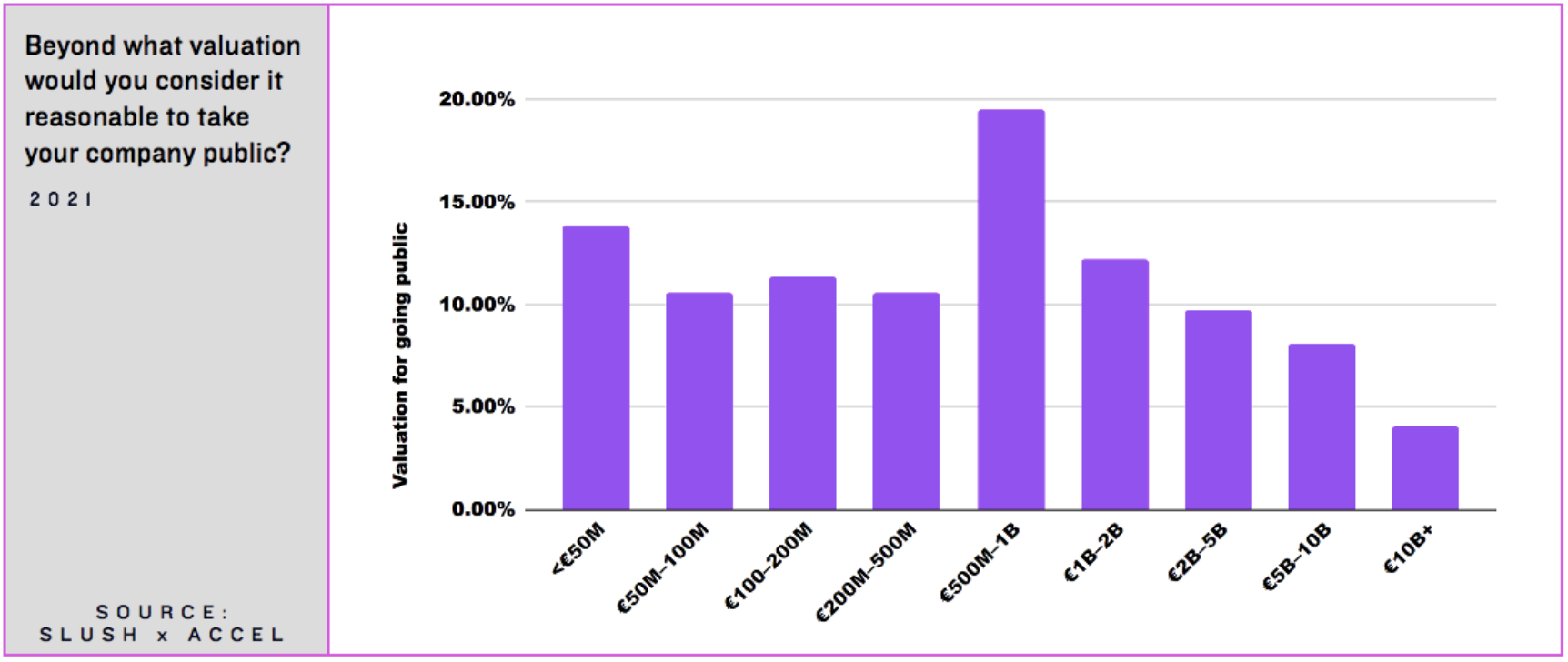

It is hardly surprising that when it comes to valuation, the greatest concentration in the data (19.5%) is around the €1B mark of unicorn status that has become a strong informal metric of success within the global startup ecosystem. Nevertheless, the data is still relatively broadly distributed starting from the lowest valuation category of <€50M which has the second highest proportion (13.8%), possibly reflecting the higher variety of IPO profiles in Europe.

When compared with Dealroom data on actual IPO valuations, we can see that European founders have a quite accurate understanding of the general valuation levels at which companies IPO in Europe. The median in our data, €500M-1B, is around the average valuation at which European companies have IPO’d according to Dealroom data, €699.2M.

* Here 2021 data refers to data from Dealroom up to the end of April 2021.